China's latest wave of overseas expansion is taking place in a markedly different environment from previous globalization cycles, according to a new report released in Shanghai, as Chinese companies face growing geopolitical tensions, shifting trade rules and rising protectionism.

The 2026 China Eng Global Influence Report, jointly released by the China Enterprise Globalization Alliance (CEGA) and the Jiemian Cailian Intelligence Institute, argues that the success of Chinese companies abroad can no longer be measured solely by financial performance. Instead, firms must move beyond simply "going global" and learn how to "grow local" in overseas markets.

The report was unveiled during the 2026 China Enterprises Global Impact Dialogue, held in Shanghai's Xuhui district on June 12-13.

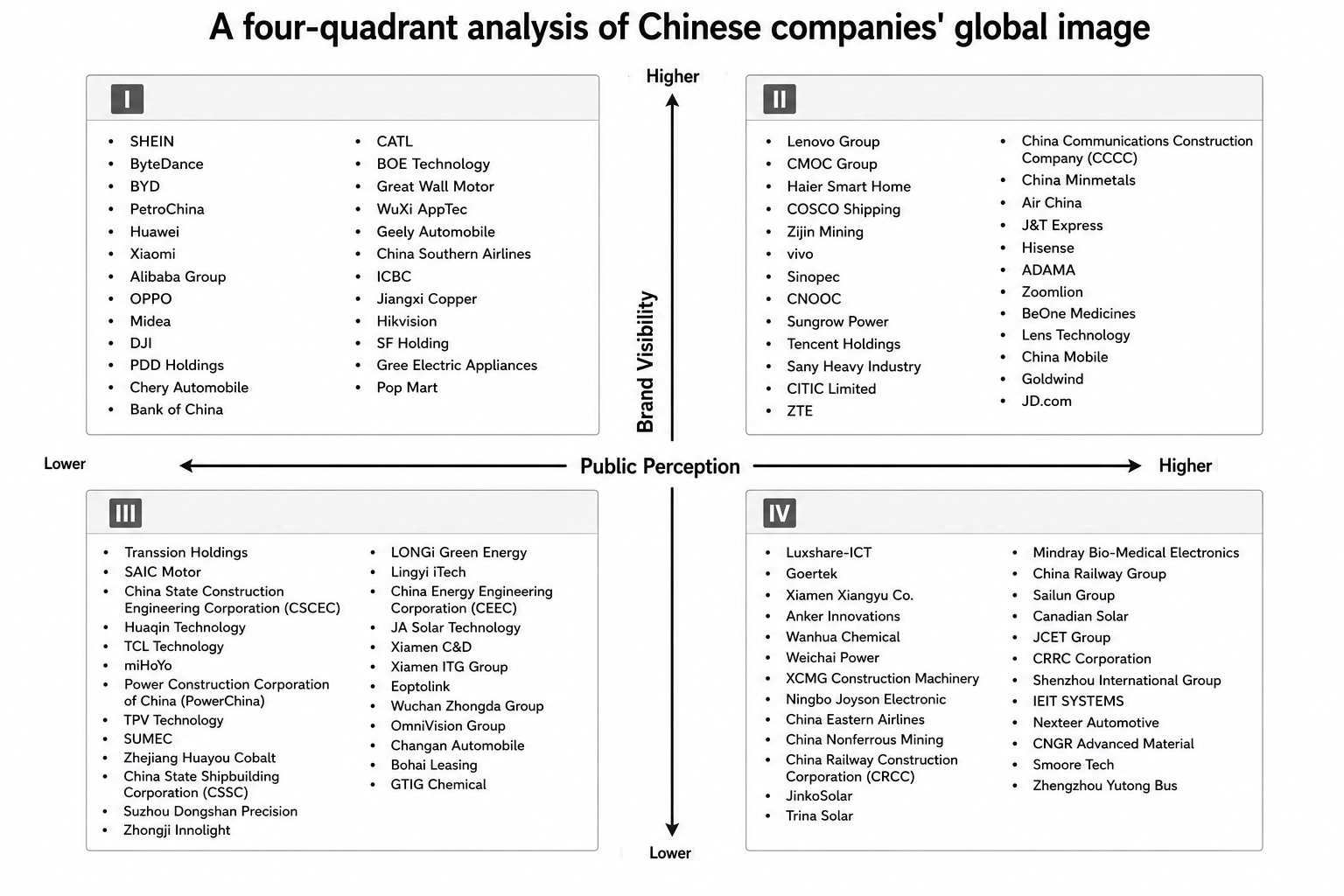

To evaluate companies' international standing, the report developed a new assessment framework based on three core dimensions: product acceptance, brand and image recognition, and local contribution. Based on the framework and assessments by an expert panel, the organizers unveiled the "2026 China Corporate Global Influence Top 100" along with industry-specific top 10 rankings.

CUI Yu, head of the Jiemian Cailian Intelligence Institute and chief architect of the report, said the framework goes beyond conventional indicators such as market share and corporate value. It also incorporates factors including public perception, localization efforts, participation in global supply chains and fulfillment of social responsibilities.

YU Jingzhong, executive chairman of CEGA, said the framework could help companies identify strengths and weaknesses in their international operations while providing a new lens through which to assess China's broader soft-power development.

The report defines "going global" broadly, encompassing not only exports of goods and services but also overseas acquisitions, foreign manufacturing facilities, technology partnerships, localized operations and participation in global value chains.

On the trade front, the report notes that China's merchandise export growth has slowed significantly, with annual growth stabilizing around 5% and the country's share of global exports remaining between 14% and 15% for six consecutive years. Exports are increasingly shifting toward intermediate and capital goods, while the share of consumer goods continues to decline.

Service exports, meanwhile, remain on a long-term growth trajectory despite periodic fluctuations. China's service exports reached US$445.9 billion in 2024, up 17% year on year.

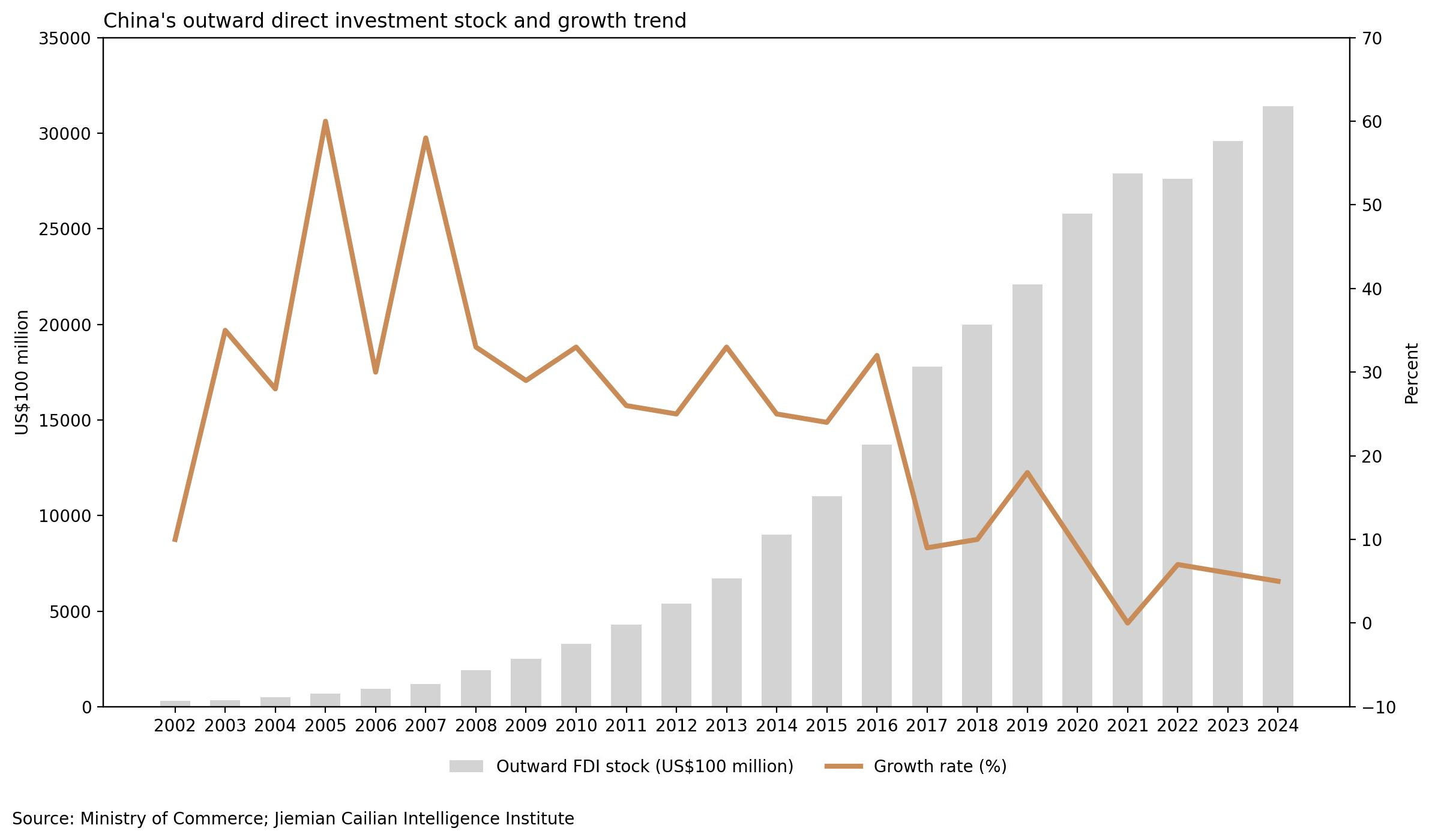

Overseas investment has also continued to expand. By the end of 2024, about 34,000 Chinese investors had established roughly 52,000 overseas enterprises with total overseas assets exceeding US$9 trillion. China's outward direct investment stock reached US$3.1 trillion, ranking third globally.

The report highlights a major shift in investment patterns. Mergers and acquisitions accounted for just 13.4% of China's outward direct investment in 2024, down sharply from a peak of 75.6% in 2017, while greenfield investment has become the dominant mode of overseas expansion.

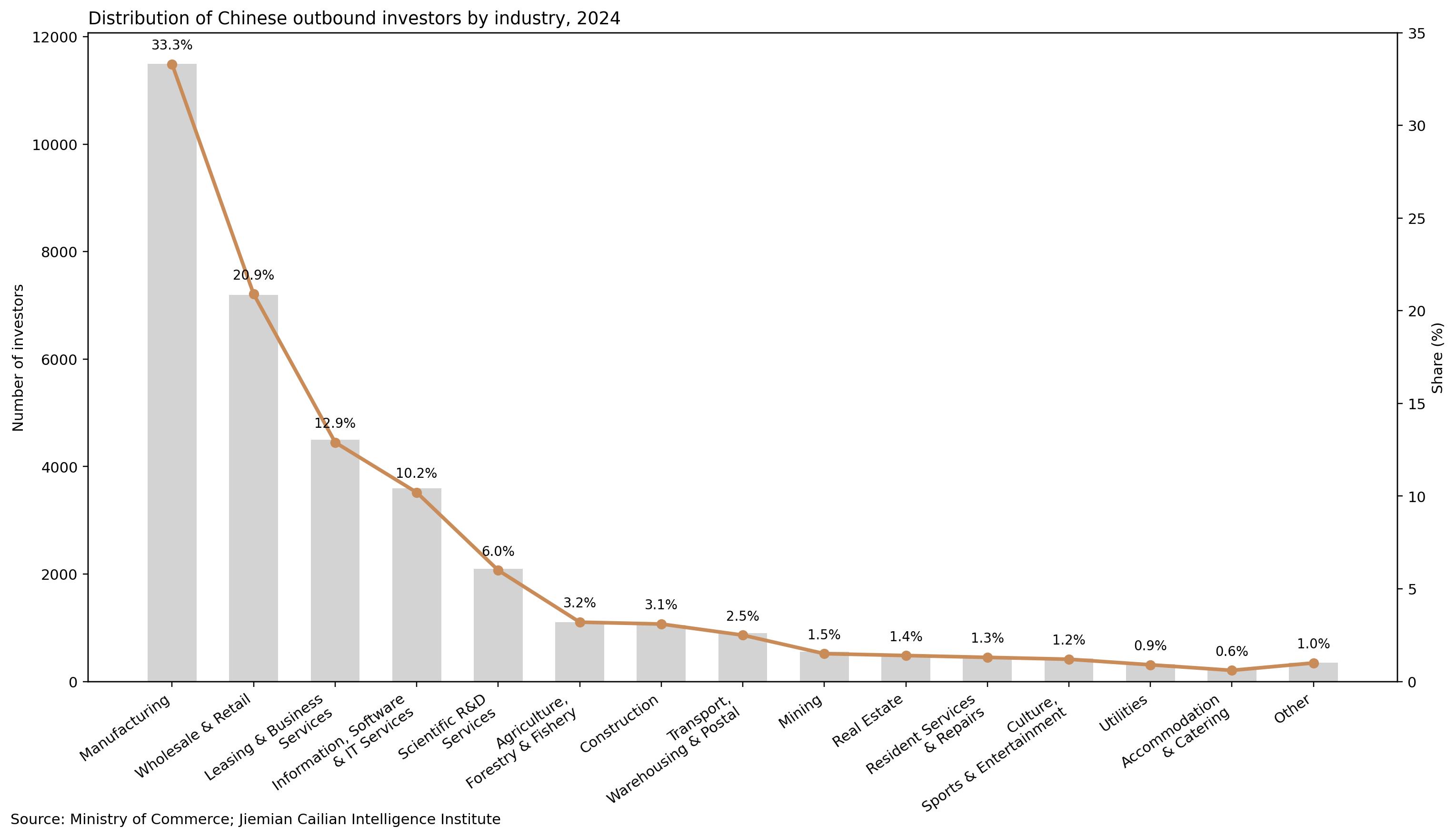

Manufacturing remains the most active sector for outbound investment despite a gradual decline in its share. In 2024, manufacturing accounted for 33.3% of Chinese outbound investors, followed by wholesale and retail trade at 20.9%.

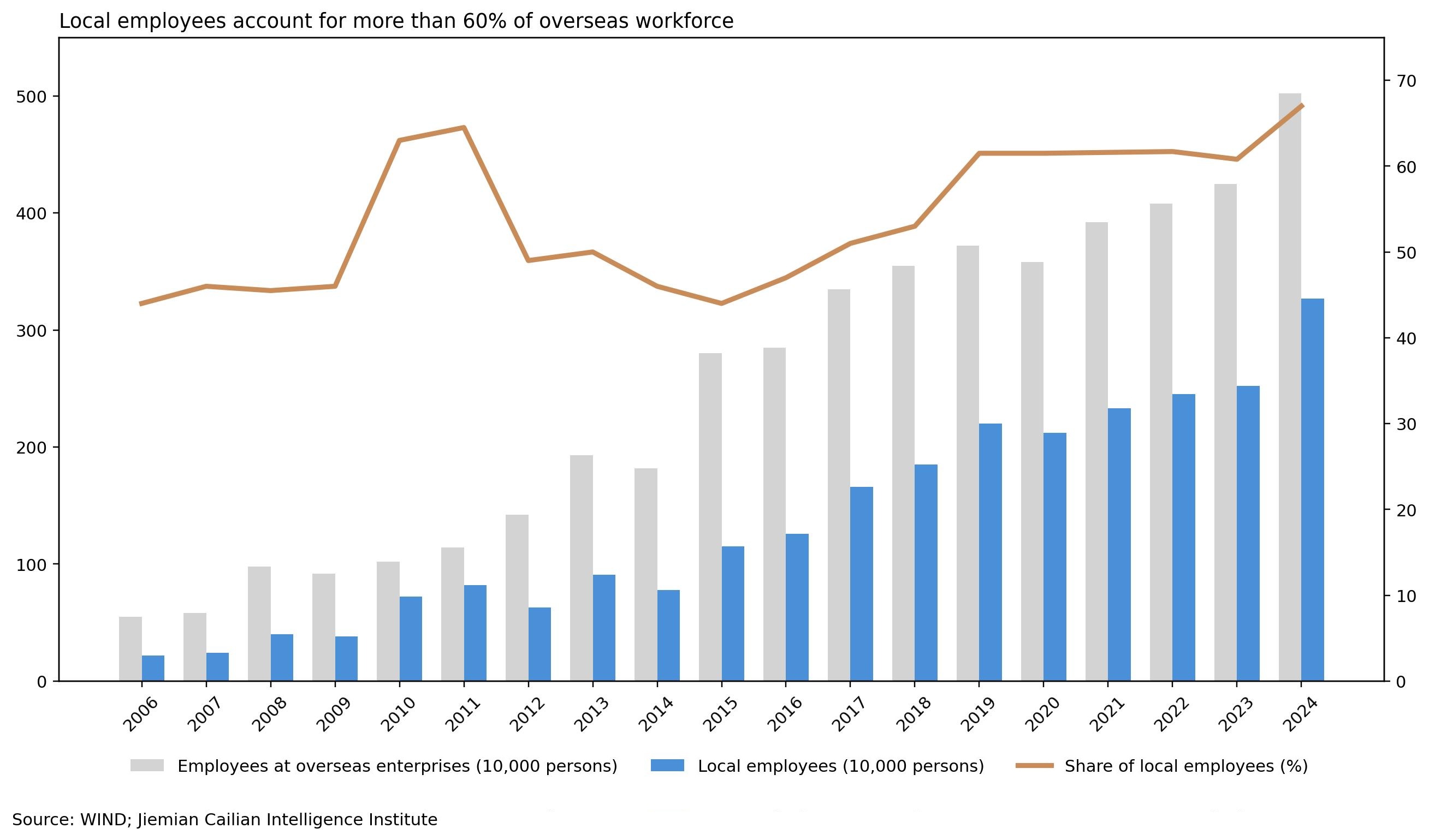

The report also points to a growing localization trend. Employment at overseas Chinese-invested companies reached 5.02 million people by the end of 2024, including 3.3 million local employees. Local hires accounted for nearly two-thirds of the workforce.

According to the report, Chinese companies are undergoing a structural shift in their overseas expansion strategies. Trade is becoming more knowledge-intensive, investment is increasingly focused on advanced manufacturing and digital industries, and market diversification is accelerating across both exports and overseas investment destinations.

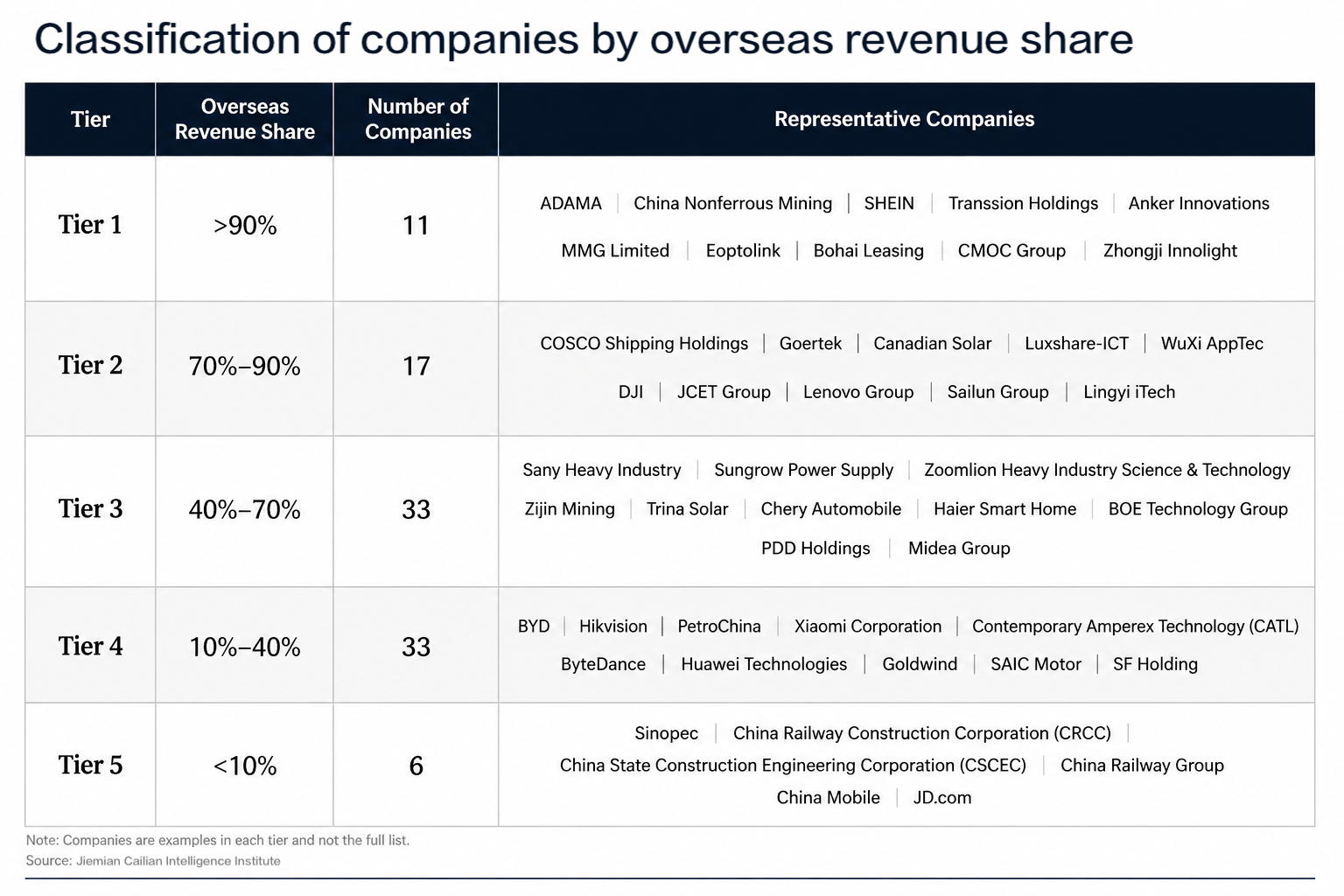

Using the Top 100 companies as a sample, the report identifies three distinct globalization models.

The first consists of highly overseas-dependent firms, where international revenue accounts for more than 70% of total revenue. Examples include Anker Innovations and SHEIN.

The second group comprises balanced global operators with overseas revenue contributing between 40% and 70% of total sales. Representative companies include Haier Smart Home and Midea Group.

The third category includes companies where overseas revenue contributes less than 40% of total sales. Representative firms include China State Construction and BYD. While these companies maintain significant international operations, the classification is based on revenue exposure rather than global footprint.

The report argues that companies should avoid relying on a single competitive advantage. Firms with strong products but limited public recognition should invest more in branding and global communications, while those with high visibility but weaker commercial performance need to strengthen product competitiveness. Companies with strong products but limited local engagement should deepen integration with local economies and communities to become long-term contributors to host markets.

Looking ahead, Cui said Jiemian Cailian Press would establish a long-term observation mechanism for representative globalizing companies and continue refining the evaluation framework through corporate participation, field research and country-specific studies.

He also emphasized the role of government support in helping companies build influence abroad. Shanghai has already established a city-level overseas expansion service platform, formed professional service alliances and expanded offline support networks. Xuhui district has launched a "New Quality Service Provider" initiative that has attracted 45 professional institutions and introduced service vouchers designed to help smaller innovative firms access specialized resources at lower cost.

"The next step is to improve the match between service supply and corporate demand," Cui said. "Shanghai has already taken the first step from zero to one. The challenge now is moving from having these resources to ensuring companies can effectively use them."